What Is A Flexible Mortgage?

Taking out a mortgage is a big commitment, and it’s essential to keep up with your monthly repayments for your agreed term or you face having your home repossessed. However, this is where flexible mortgages can help!

Flexible mortgages offer a lot of benefits and provide homeowners with more flexibility, making them a great solution if you feel like paying your mortgage off in a more irregular fashion would work for you.

To help our customers gain a better understanding of flexible mortgages and how they work, we’ve created this short guide on flexible mortgages in the UK.

What is a flexible mortgage?

Let us start by explaining exactly what a flexible mortgage is.

A flexible mortgage is as a type of mortgage that allows borrowers to make additional payments, underpayments, overpayments, and take payment holidays, all while maintaining the same mortgage terms and conditions. As the name suggests, these elements makes this type of mortgage far more flexible than standard residential mortgages.

Flexible mortgages typically have a set minimum monthly payment, but borrowers are free to pay more when they can afford to do so, reducing the overall interest they pay over the life of the mortgage.

In contrast, payment holidays or underpayments allow borrowers to reduce or suspend their monthly mortgage payments in case of unforeseen financial difficulties, without incurring any penalties.

Who are flexible mortgages for?

Flexible mortgages are best suited to:

-

Those with fluctuating incomes

-

Those with unpredictable incomings and outgoings

-

Small business owners

-

Those who expect their financial circumstances to change over the term of the mortgage

Some flexible mortgages also offer offset facilities, which allow borrowers to use their savings or current account balances to offset their mortgage balance, further reducing the interest charged.

Flexible mortgages can be more complex and may have higher interest rates or fees, but they offer the flexibility to adapt to changing financial circumstances and can help borrowers pay off their mortgage sooner.

.jpg)

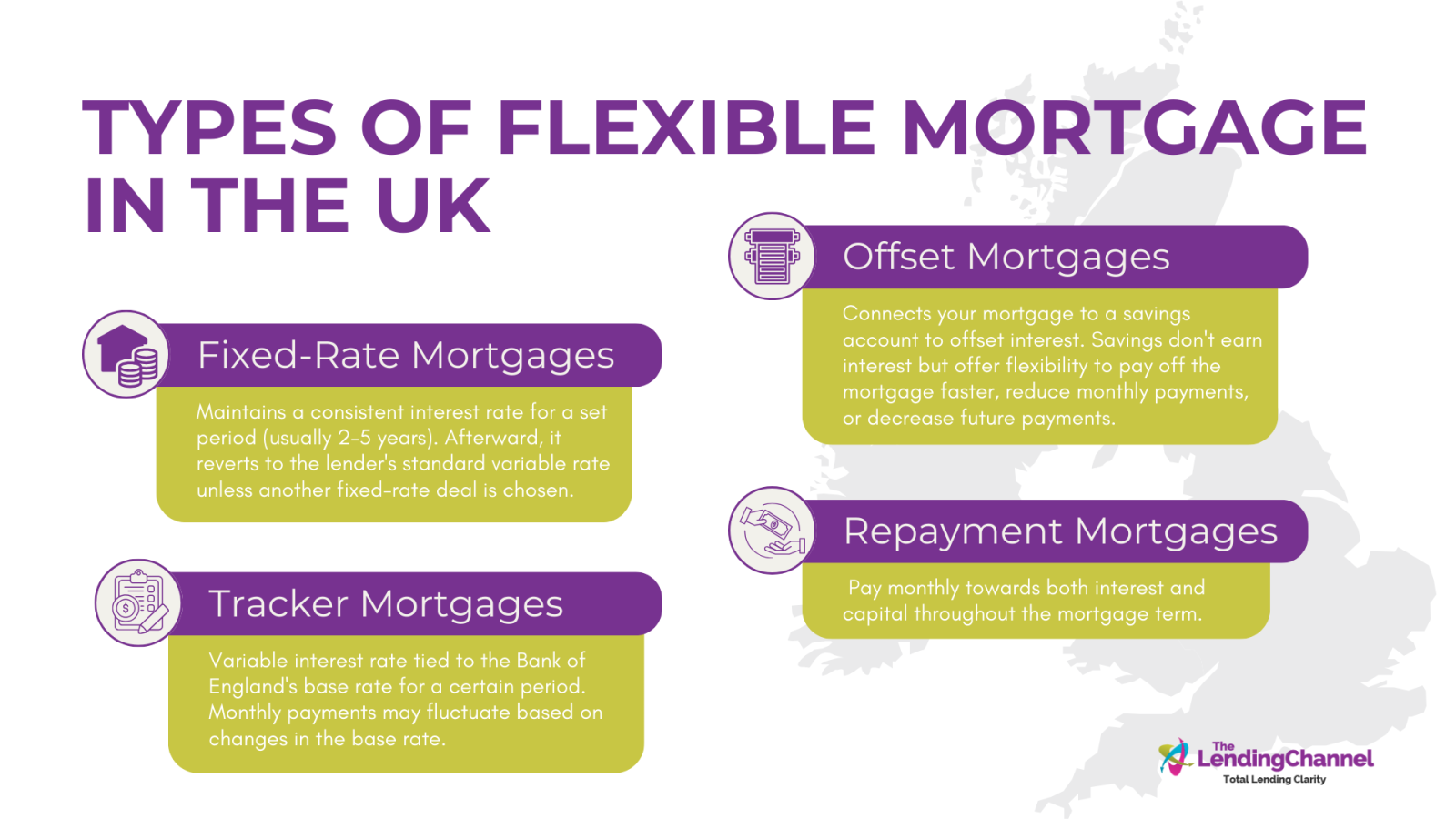

What are the types of Flexible Mortgage UK?

There are a few different types of Flexible Mortgage to choose from, all of which we've outlined below.

Flexible Repayment Mortgages

A flexible repayment mortgage, also known as a capital repayment mortgage, enables you to make monthly payments towards both the interest and capital amount throughout the term of your mortgage.

Flexible Offset Mortgages

A flexible offset mortgage is a home loan that is connected to a savings account. The funds in the savings account are utilized to offset the mortgage interest on your monthly repayments. With an offset mortgage, your savings will not earn interest, but you have the flexibility to choose from the following options: pay off your mortgage quicker, lower your monthly repayments, or decrease your future mortgage payments.

Flexible Fixed-Rate Mortgages

A flexible fixed-rate mortgage maintains a consistent interest rate for a specified duration of time. Typically, the fixed-rate term of a mortgage is between two to five years, but some providers may offer up to 10 years. After the fixed-term period concludes, the mortgage will revert to the lender's standard variable rate (SVR) unless you opt for another fixed-rate deal.

Flexible Tracker Mortgages

A flexible tracker mortgage is a type of loan that comes with a variable interest rate, which means that your monthly payments may go up or down. Typically, this mortgage type follows the interest rate of the Bank of England's base rate for a specified duration. If the base rate increases, your interest rates are likely to go up, resulting in higher repayments. Conversely, if the base rate drops, the interest on your repayments may become more affordable.

Every type of flexible mortgages follows the same basic principles of being more adaptable to changing financial situation. The type of flexible mortgage you choose will impact your repayment rates, interest rates and loan term.

What are the advantages of flexible mortgages?

As the name suggests, flexible mortgages offer a higher level of flexibility in terms of monthly repayments, which can help homeowners who have fluctuating or unpredictable income manage their repayments in a more suitable. way for their unique circumstance.

Some of the main advantages of flexible mortgages are:

-

The option to make overpayments to pay your mortgage back faster

-

Underpayments and payment holidays can be used if a borrower has an unexpected expense or a reduction in income – this means borrowers can reduce their monthly payments or stop making payments for a short period of time, without incurring penalties.

-

Interest is calculated on a daily or monthly basis, rather than annually meaning that borrowers can save money on interest by making overpayments, as the additional payments reduce the outstanding balance immediately and reduce the interest charged on the remaining balance.

-

You could switch to a fixed-rate mortgage without early repayment penalties or having to remortgage.

Potential drawbacks of flexible mortgages

Despite the many advantages of flexible mortgages, they are not perfect and they are not suited for everyone. Depending on your financial situation and goals, you may find that a more rigid repayment structure works better for you.

In addition, flexible mortgages can incur higher interest rates and be more complex to manage. The main cons of flexible mortgages are:

-

Interest will keep being charged during any payment breaks, meaning your overall payment might be larger at the end of your term.

-

Often have higher interest rates compared to traditional mortgages, which means you may end up paying more in interest over the life of the loan.

-

Flexible mortgages are not offered by all lenders, which can limit your options.

-

Can be more complex than traditional mortgages, with different features such as overpayment allowances, underpayment options, and redraw facilities. This complexity can make it harder to understand the terms of the loan and how to use the features to your advantage.

-

Flexible mortgages tend to come with higher fees attached, such as arrangement fees, valuation fees, and early repayment charges.

What are overpayments?

Most mortgages require you to make the same regular monthly payment, with no option to over or underpay. Flexible Mortgages allow you to make additional payments on top of your regular ones. This helps you reduce your balance, as well as save on interest. And perhaps best of all, you’ll pay your mortgage off much quicker.

You can make this payment as a lump sum (if, for example, you wanted to top your repayment up with a large inheritance payment) or as a smaller chunk.

You also have the option to regularly overpay by setting up a standing order. As this is totally voluntary, the overpayment can be cancelled at any time.

Remember, depending on your lender, there may be a cap on the amount you can overpay each year.

If you’re planning on making a habit of overpaying, make sure you seek mortgage advice from registered mortgage broker professionals, like The Lending Channel, before committing to anything.

What are underpayments?

Underpayments are when you pay less than your regular monthly mortgage re-payment, allowing borrowers to manage their outgoings more effectively for situations where they face a month with several high payments.

In the same way that you have the option to overpay, you may also be able to underpay for a set period of time. Subject to prior approval from your lender, this can help you manage your finances better and allow you some short-term leeway, should you need it.

However, please note that most of the time the amount you can underpay and the length of time your lender will agree to will be almost entirely dependent on how much you’ve previously overpaid.

What are flexible mortgage payment holidays?

A payment holiday, or “mortgage holiday” is essentially a short break in your repayments. Homeowners can take a holiday from their regular monthly payments to manage their costs in a more effective way.

Pausing your mortgage can be extremely useful especially if you’re planning a trip, having a baby or helping a relative to purchase their first home. It’s a short term solution that can make a big difference to your monthly outgoings.

The length of time you’ll be permitted to take a break will depend on your lender, but generally, it could last between 1 and 6 months.

To take a payment break, there is often an application process. Your acceptance might hinge on your history of reliability and whether you’ve overpaid enough to cover the break. It’s important to note that your interest will still accumulate during this time, so you will likely come back to an increased amount once your break is over.

Interest rates calculated daily

Having your interest calculated daily rather than yearly or monthly is, overall, the most cost-effective method. Any payments you make are immediately taken off your total - and the lower the amount, the less interest you’ll have to pay.

This means that any overpayments you make are sure to make a visible difference immediately.

Flexible Mortgage Savings Account

Choosing a Flexible Mortgage gives you the option to 'borrow back' the money that you’ve overpaid into your mortgage. It’s essentially like a pot of money that you can dip into in the future should you need it.

Can you switch your type of flexible mortgage?

Yes, with flexible mortgages borrowers have the option of switching their mortgage type during their term.

Switching allows you to switch to different types of flexible mortgages. You can do this without incurring early repayment charges or having to reapply.

Are flexible mortgages portable?

Notably, if you move properties, some lenders will give you the option to move your Flexible Mortgage with you. This saves time and stress, and you won’t have to reapply for a mortgage or incur any early repayment charges.

Let us help find the perfect Flexible Mortgage for you

Flexible Mortgages can be an excellent option for many people, but it’s important to know exactly what will work for you. Our expert team can provide all the help and advice you need on flexible mortgages, as well as on other finance products, such as invoice finance, asset finance and equity release.

The Lending Channel tea are well-versed in finding the best deals for your specific needs and requirements and will be happy to take you through each of your options and discuss them in detail, answering any outstanding questions you may have.

Our team has years of experience in specialist mortgage comparison, and we’re confident that we can find the right type of mortgage for you, flexible or otherwise.

To find out more about flexible mortgages or to elicit our help on another one of our financial products, do not hesitate to get in touch today.

.jpg)

.png)